Introduction

There are an estimated 26 million micro and small enterprises (MSEs) in the country providing employment to an estimated 60 million persons. The MSE sector contributes about 45% of the manufacturing sector output and 40 % of the nation’s exports. Of all the problems faced by the MSEs, non- availability of timely and adequate credit at reasonable interest rate is one of the most important. One of the major causes for low availability of bank finance to this sector is the high risk perception of the banks in lending to MSEs and consequent insistence on collaterals which are not easily available with these enterprises. The problem is more serious for micro enterprises requiring small loans and the first generation entrepreneurs.

The Credit Guarantee Fund Scheme for Micro and Small Enterprises (CGMSE) was launched by the Government of India to make available collateral-free credit to the micro and small enterprise sector. Both the existing and the new enterprises are eligible to be covered under the scheme. The Ministry of Micro, Small and Medium Enterprises and Small Industries Development Bank of India (SIDBI), established a Trust named Credit Guarantee Fund Trust for Micro and Small Enterprises (CGTMSE) to implement the Credit Guarantee Fund Scheme for Micro and Small Enterprises. The scheme was formally launched on August 30, 2000 and is operational with effect from 1st January 2000. The corpus of CGTMSE is being contributed by the Government and SIDBI in the ratio of 4:1 respectively and has contributed Rs.1906.55 crore to the corpus of the Trust up to March 31,2010. As announced in the Package for MSEs, the corpus is to be raised to Rs.2500 crore by the end of 11th Plan.

Eligible Lending Institutions.

The institutions, which are eligible under the scheme, are scheduled commercial banks (Public Sector Banks/Private Sector Banks/Foreign Banks) and select Regional Rural Banks (which have been classified under ‘Sustainable Viable’ category byNABARD). National Small Industries Corporation Ltd. (NSIC), North Eastern Development Finance Corporation Ltd. (NEDFi) and SIDBI have also been made eligible institutions. As on March 31, 2010, there were 112 eligible Lending Institutions registered as (MLIs) of the Trust, comprising of 27 Public Sector Banks, 16 Private Sector Banks, 61 Regional Rural Banks, 2 Foreign Bank and 6 other Institutions viz., NSIC, NEDFI, SIDBI and The Tamil Nadu Industrial Investment Corporation(TNIIC).

Eligible Credit Facility

The credit facilities which are eligible to be covered under the scheme are both term loans and working capital facility up to Rs.100 lakh per borrowing unit, extended without any collateral security or third party guarantee, to a new or existing micro and small enterprise. For those units covered under the guarantee scheme, which may become sick owing to factors beyond the control of management, rehabilitation assistance extended by the lender could also be covered under the guarantee scheme. It is noteworthy that if the credit facility exceeds Rs.50 lakh, it may still be covered under the scheme but the guarantee cover will be extended for credit assistance of Rs.50 lakh only. Another important requirement under the scheme is that the credit facility

should be availed by the borrowing unit from a single lending institution. However, the unit already assisted by the State Level Institution/NSIC/NEDFi can be covered under the scheme for the credit facility availed from member bank, subject to fulfillment of other eligibility criteria. Any credit facility in respect of which risks are additionally covered under a scheme, operated by Government or other agencies, will not be eligible for coverage under the scheme.

Guarantee Cover

The guarantee cover available under the scheme is to the extent of 75 percent of the sanctioned amount of the credit facility. The extent of guarantee cover is 80 per cent for (i) micro enterprises for loans up to Rs.5 lakh; (ii) MSEs operated and/or owned by women; and (iii) all loans in the North-East Region. In case of default, Trust settles the claim up to 75% (or 80% wherever applicable) of the amount in default of the credit facility extended by the lending institution. For this purpose the amount in default is reckoned as the principal amount outstanding in the account of the borrower, in respect of term loan, and amount of outstanding working capital facilities, including interest, as on the date of the account turning Non-Performing Asset (NPA).

Tenure of Guarantee

The Guarantee cover under the scheme is for the agreed tenure of the term loan/composite credit. In case of working capital, the guarantee cover is of 5 years or block of 5 years.

Fee for Guarantee

The fee payable to the Trust under the scheme is one-time guarantee fee of 1.5% and annual service fee of 0.75% on the credit facilities sanctioned. For loans up to Rs.5 lakh, the one-time guarantee fee and annual service fee is 1% and 0.5% respectively. Further, for loans in the North-East Region, the one-time guarantee fee is only 0.75%.

Website

Operations of CGTMSE are conducted through Internet. The website of CGTMSE has been hosted at www.cgtsi.org.in. Scheme Awareness Programmes

CGTMSE has adopted multi-channel approach for creating awareness about its guarantee scheme amongst banks, MSE associations, entrepreneurs, etc. through print and electronic media, by conducting workshops/seminars, attending meetings convened at various district/state/national fora, etc. As on March 31,2010, 1080 workshops and seminars were conducted on Credit Guarantee Scheme. Also, CGTMSE participated in 19 exhibitions and attended 304 SLBC/meetings convened by RBI/other Government offices. Posters and mailers have been circulated to banks, industry associations, and other stakeholders for promoting the scheme and creating its greater awareness. With a view to imparting training to MLIs through their training colleges, multimedia CD-ROM containing operational modalities of the scheme, was distributed to the staff training centers/colleges of the MLIs. The Trust has recently launched an advertisement campaign in 194 newspapers across the country through DAVP, which has created considerable awareness about the scheme among the target audience. Operational Highlights of CGTMSE

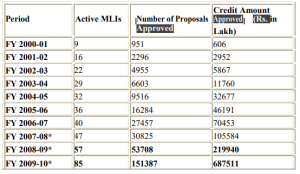

Operational Highlights of CGTMSE

As on March 31, 2010, 3,00,105 proposals from micro and small enterprises have been approved for guarantee cover for aggregate credit of Rs.11550.61 crore, extended by 85 MLIs in 35 States/UTs. A year-wise growth position is indicated in the table below:

Scheme of Micro Finance Programme

The Government has launched a Scheme of Micro Finance Programme in 2003-04.The Scheme has been tied up with the existing programme of SIDBI by way of contributing towards security deposits required from the MFIs/NGOs to get loan from SIDBI.The scheme is being operated in underserved States and underserved pockets/districts of other states. The Government of India provide funds for Micro-Finnance Programme to SIDBI, which is called ‘Portfolio Risk Fund'(PRF).At present SIDBI takes fixed deposit equal to 10% of the loan amount.The share of MFIs/NGOs is 2.5% of the loan amount (i.e. 25% of security deposit) and balance 7.5%(i.e. 7.5% of security deposite) is adjusted from the funds provided by the Government of India. As on 31st March 2010, the Government has released an amount of Rs.80.00 crore towards ‘Portfolio Risk Fund'(PRF).An amount of Rs .6.00 crore has been released during 2009-10. As on 31st march 2010,cumulative loan amount of Rs.1299.68 crore has been provided to MFIs/NGOs under the Scheme benefiting approximately 20.21 lakh persons. Of this,more than 80% are estimated to be women beneficiaries.